All You Need to Know About Grace Periods for Borrowers

May 15, 2024 By Susan Kelly

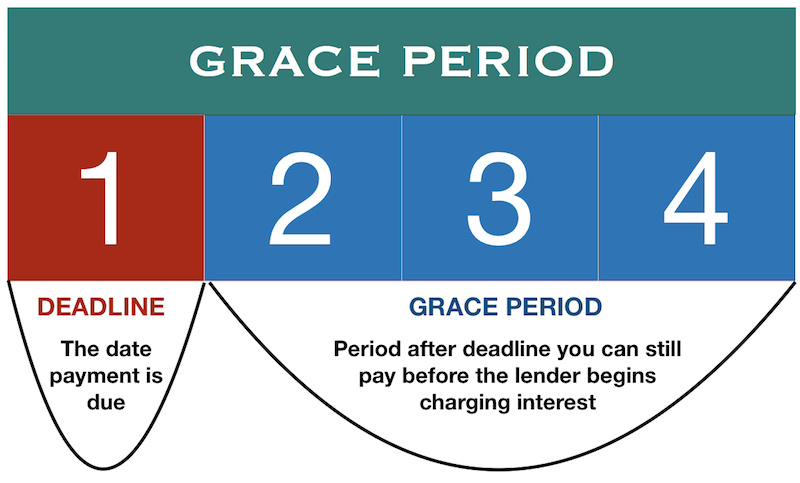

A time of grace is a set period when a person who borrowed money can delay making their payment on a loan or credit card without any punishment. It works like an economic protection net, giving the borrower some space to deal with short-term cash flow difficulties or sudden costs. Understanding how grace periods work gives people control over smartly managing financial duties. They pay on time but also protect their good credit standing. So, to keep the economy stable and strong we must understand how grace periods work.

Definition of Grace Period

A time, which can be from a few days to one month, relies on the choice of the lender and the kind of financial agreement. This period of flexibility protects borrowers from extra charges for being late and keeps their credit position intact. But, it is important to understand that even though no fines are charged for being late with a payment, interest might still increase on your remaining balance.

Looking at the expansion in time, grace periods can also act as a defense against unforeseen money problems. If someone has a medical emergency or loses their job unexpectedly, it may be difficult for them to pay on time. Grace periods give borrowers some space to handle these emergencies without having immediate impacts on their finances.

- Interest Accrual: Interest may still accumulate during the grace period, impacting the overall repayment amount.

- Credit Score Protection: Grace periods prevent missed payments from tarnishing borrowers' credit scores, ensuring financial stability.

How Do Grace Periods Work?

Grace periods work like a tactical buffer for those who borrow money, giving them a better way to handle their financial commitments. Imagine you have a credit card statement that should be paid by the 15th and it comes with 25 days grace period. This gives users enough time to pay off all dues, stretching flexibility beyond just one billing cycle.

In addition, grace periods help those who borrow money to concentrate on their financial duties. This promotes improved budget control and money-handling skills. Learning about the workings of a grace period can assist people in using this time frame skillfully to manage their finances well.

- Payment Prioritization: Grace periods enable borrowers to allocate funds strategically, addressing pressing needs before payment deadlines.

- Budget Flexibility: Understanding grace periods aids in crafting flexible financial plans, and accommodating unforeseen expenses or income fluctuations.

Benefits of Grace Periods

Grace periods are like a temporary safe place in moments of money pressure. They protect those who borrow from any punishments and create a feeling of financial safety. Especially in times when the economy is not stable, this flexibility can save people who have been hit by unexpected money problems.

Additionally, grace periods give people who borrow money a chance to find other financial options like combining their debts or renegotiating them. This is possible because they have more time without any immediate deadlines. It helps in taking actions that can reduce future financial risks and make handling debt easier.

- Financial Resilience: Grace periods provide a buffer against financial shocks, enabling borrowers to weather economic uncertainties with greater resilience.

- Debt Management Strategies: Leveraging grace periods strategically can pave the way for proactive debt management, fostering long-term financial health.

Examples of Grace Periods

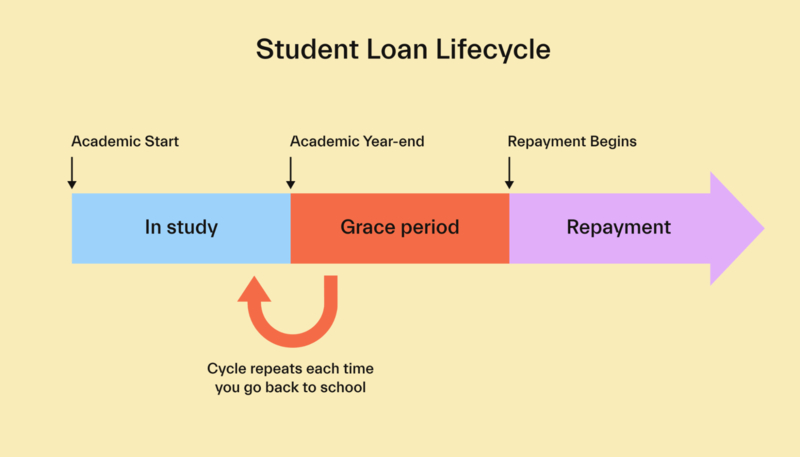

Imagine a mortgage loan that has a grace period of 15 days. If you have to make your payments on the 1st, this means borrowers can settle their dues without any penalty until they reach or pass by the 15th day. Similarly, if we talk about a student loan that provides a grace period of 30 days, it indicates that you still have time to pay even after crossing your initial due date.

Moreover, grace periods are found not only in loans but also in many other financial arrangements like utility bills and insurance premiums. Knowing about these situations helps to show how grace periods work in different areas of finance.

- Utility Bills: Many utility providers offer grace periods to customers, allowing for flexibility in bill payments without immediate repercussions.

- Insurance Premiums: Grace periods in insurance policies provide policyholders with additional time to pay premiums, preventing lapses in coverage.

Factors to Consider

Grace periods are a helpful break for the person getting the loan, but it is very important to carefully look at all details in agreements about loans. Differences in how long grace periods last or if there's no grace period can change how much it costs to borrow money quite a lot. Also, when interest piles up during this time frame, it highlights why making payments on time matters so much for lessening future financial pressures.

Moreover, those who borrow money need to understand that if they don't pay back what was borrowed within the given grace period, it might affect their credit scores for a long time. If people consider these things carefully, they can make educated choices about the money they owe and ensure stability in their financial lives while also reducing unwanted expenses.

- Credit Score Implications: Late payments beyond the grace period can negatively impact credit scores, affecting future borrowing capabilities.

- Loan Terms: Understanding the terms and conditions of loans is crucial, as variations in grace periods and interest accrual can impact overall repayment obligations.

Conclusion

In conclusion, grace periods offer a crucial safety net for borrowers, granting them essential breathing space amidst financial commitments. This temporal leniency empowers individuals to navigate unforeseen challenges with greater resilience, fostering financial stability in the face of adversity. By comprehensively grasping the mechanics of grace periods and their broader implications, borrowers can proactively steer their financial journey, making astute decisions tailored to their unique circumstances. Embracing this facet of financial management not only promotes fiscal discipline but also cultivates a deeper sense of financial literacy, empowering individuals to navigate the complex landscape of borrowing with confidence and prudence.

How My 401(k) Investments Affect Take Home Pay

Your total taxable income will be lower because your contributions are deducted before taxes, resulting in a smaller tax bill for you. However, the amount of your take-home income that is decreased will be less than what you contribute.

Feb 21, 2024 Triston Martin

Understanding Reverse Mortgage Refinancing

This article explores the concept of refinancing a reverse mortgage in simple terms, explaining the process, benefits, and considerations

Oct 17, 2023 Susan Kelly

Why Does Getting a Mortgage Take So Long

Frustrated by how long it takes to get approved for a mortgage? We explore why, highlighting all the paperwork, processes, and regulations involved in applying for a loan.

Feb 21, 2024 Susan Kelly

Pledged Asset

A pledged asset refers to a valuable property given to a lender in return for a loan or debt. Lenders hold collateral in exchange for loan funds, a pledge asset. A lender may reduce the down payment required to obtain a loan and the interest rate by pledging assets. You can pledge cash, stocks, bonds, and other equity or securities.

Dec 01, 2023 Triston Martin

Cabela's CLUB Mastercard

Apart from getting points for Cabela's as well as Bass Pro Shops purchases, cardholders enjoy special benefits and discounts.

Nov 07, 2023 Triston Martin

Your Guide to an Income Statement

Uncover the essentials of understanding and using income statements for successful financial examination and profit optimization.

May 19, 2024 Triston Martin